The speed with which a tax-cutting government has turned into a tax-raising one has caught us all unawares. In the process, there’s been little time to reflect on the shape of the strategy for raising direct taxes on income and how it affects the incomes of people at different levels of earnings. But it’s important to do so, as this year’s Autumn Statement is designed to set taxation patterns for years to come.

The most eye-catching reversal is straightforward: for the richest few percent earning six-figure sums, the top rate of 45% will not be abolished as in the doomed minibudget but in contrast extended to those ‘only’ earning £125,000 rather than £150,000. So the richest are to lead the way in paying more tax, rather than less tax.

More fundamental, though, is the decision to raise income taxes for all of us by freezing personal allowances, which are now set to have remained unchanged for a total of seven years: from April 2021 to April 2028. As has been widely pointed out, this policy during a period of inflation and nominal earnings growth means that a higher proportion of what people earn will be taxed. On current forecasts, prices will have risen 20% and earnings 22% over the period the freeze is in place, by 2027/28. This will mean everyone earning above £12,570 in 2021 pounds paying £800 more tax and NI a year than if the allowances rose in line with inflation.

Among taxpayers, this is a ‘regressive’ measure: those earning least lose relatively more of their income, because the loss is the same flat-rate amount for everyone who pays tax. Each £1 cut in the allowance costs everyone 32p, since they must pay 20p tax and 12p NI on a pound more of their income.

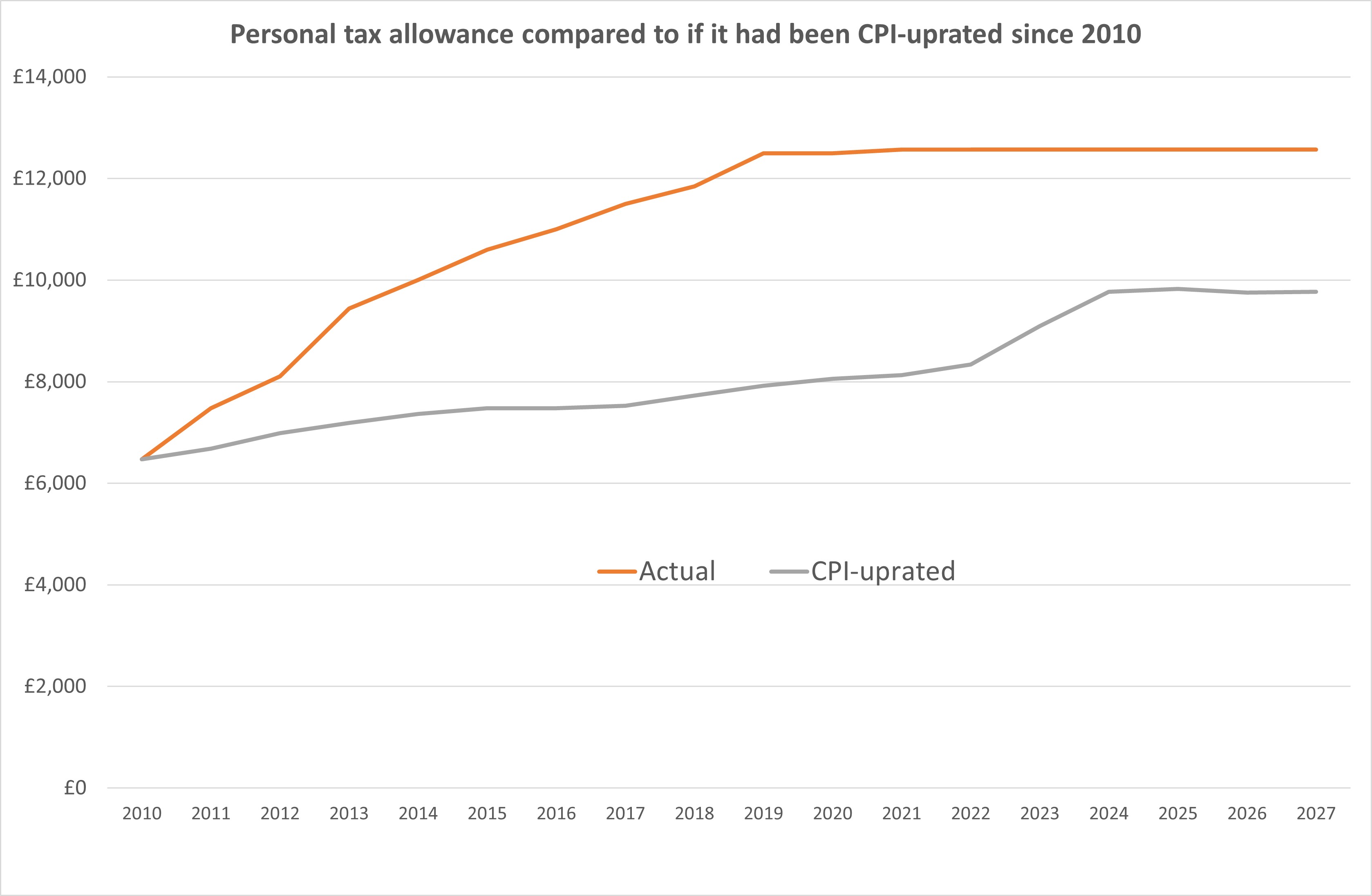

To me the most striking thing about the government choosing to reduce the value of allowances over a seven-year period is that previous Conservative chancellors have spent the past decade making a virtue of doing the opposite. Its rapid increasing of the tax allowance from £6,475 in 2010 to £12,500 in 2019 also had a flat-rate effect on taxpayers, but in a more progressive direction. Compared to previous tax cuts by (mainly Conservative) governments since the 1980s, which focused on cutting headline tax rates, it was more progressive by benefitting lower earning taxpayers comparatively more – albeit doing nothing for those on the lowest incomes who don’t pay tax.

That increase in the tax allowance since 2010 was dramatic, and the following graph shows that the current freeze does not fully undo that policy. However, it reduces the overall benefit to taxpayers (the gap between an allowance linked to inflation since 2010 and the actual tax allowance) by 40%, and there is every chance that continued pressure on the public finances after 2027 will erode these gains further.

The logical question that arises from this is clear: if the government previously saw the benefits of cutting taxes through higher allowances rather than lowering tax rates rate because it is more progressive, why has it now targeted allowances rather than tax rates as a means of raising taxes, given that this is more regressive?

The obvious answer lies in politics, to which I’ll return later. Meanwhile, here’s a pub quiz question: who was the last Chancellor to increase the basic rate of income tax, and when?

Before I tell you the answer, let’s consider briefly what would have happened last week if Jeremy Hunt had increased tax rates rather than freezing allowances.

For this purpose, let’s compare how much extra tax people would be paying now if either the tax allowance cut were already in place (this would cost us each just under £700 in 2022 prices) or by increasing all income tax rates to raise the same amount. I reckon this would require a 3 or 4 percentage points increase (eg a 23.5% basic rate, 43.5% higher rate 48.5% top rate). While that may seem quite steep, it would simply redistribute the additional amounts that various taxpayers would be liable for. Here are some examples.

A low paid part time worker earning £12,570 a year would lose nothing from the higher tax rate, (since at this personal allowance level you pay no tax) compared to £700 from the allowance cut.

A full time worker on the National Living Wage, earning about £18,500, would lose only about £200 from raising the basic rate to 23.5%, less than a third of the £700 from the allowance cut.

Someone on median full-time earnings would lose almost exactly the same amount from both policies.

A better-off worker earning £50,000 pays £1,300 more with the tax rate hike, nearly twice what they’d incur from the lower allowance.

In short, people with below median earnings would be better off, some by quite a lot, and those with higher salaries would contribute more, if income taxes were raised through rates rather than allowances.

Yet the idea of raising basic tax rates remains taboo. The amazing answer to my quiz question: the last Chancellor to raise the basic tax rate was Denis Healy in 1975. (However, several Chancellors since then have increased National Insurance rates to achieve a similar end through more politically palatable means, though this imposes more strain on working people by exempting pensioners.)

Yet in changing times, might this taboo be broken? The public appears in recent years to have become more supportive of increases in income tax rates, for all but the lowest-earning taxpayers. The language of this budget will have helped drive home the need for broadly based additional taxation : the freezing of allowances by Jeremy Hunt could hardly be called a stealth tax, as similar measures were labelled under Gordon Brown. New Labour felt obliged to perform this form of ‘fiscal drag’ rather quietly, whereas Mr Hunt could not have been more up front about the fact that this means everyone will be sharing the burden of higher taxation.

Income tax isn’t the only way to do this: wealth taxes, particularly on housing, could also play a part. But if further revenues are needed, an increase headline in tax rates, initially small, may not be out of the question. This is, after all, the tax-raising measure whose fairness is easiest to understand. Quite simply, we share out the added burden in direct proportion to our incomes. What could be fairer than that?